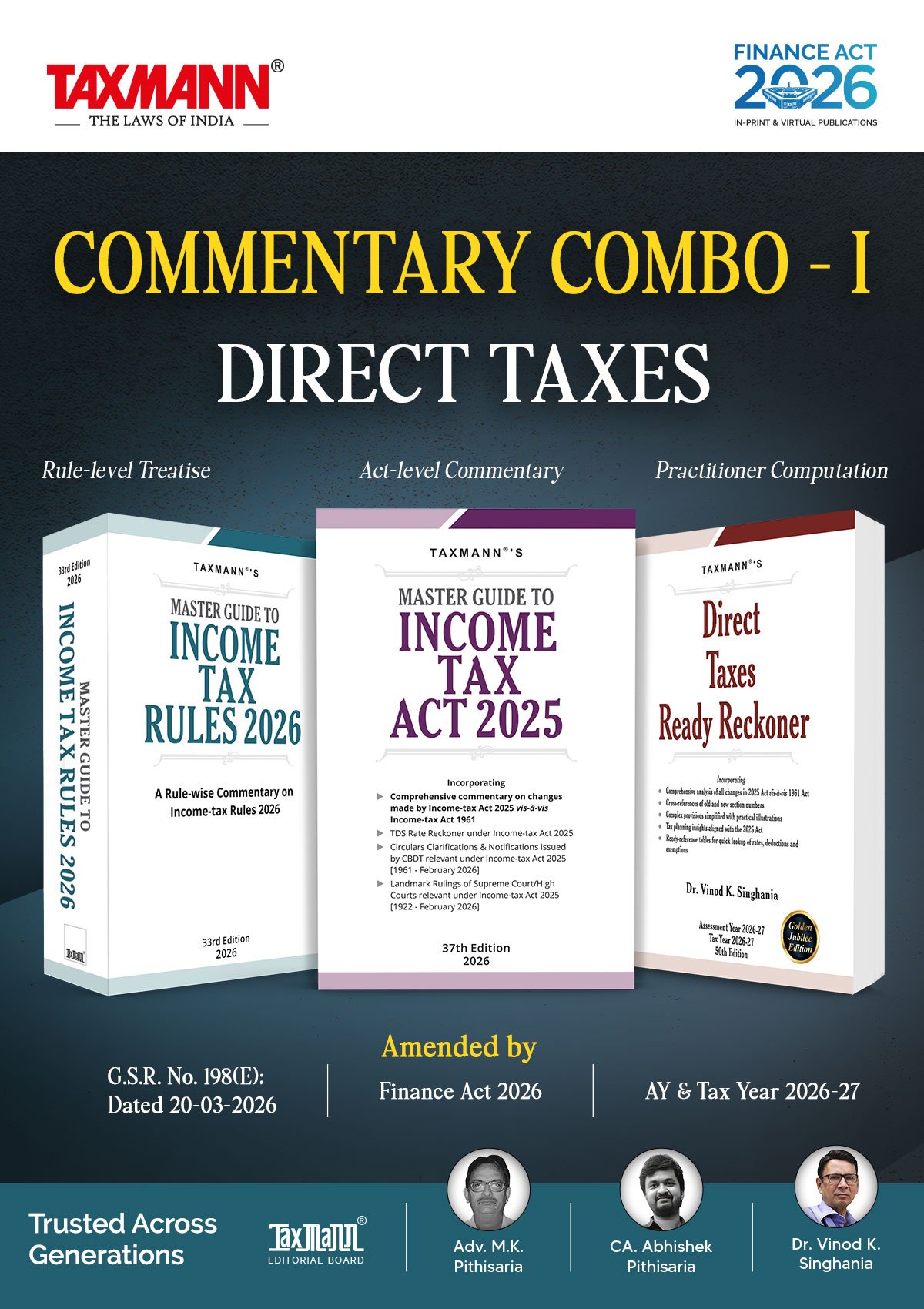

Taxmann Combo for Direct Taxes By Vinod K. Singhania 2026 Taxmann Combo for Direct Taxes By Vinod K. Singhania 2026 Description The Present Publication is the 2026 Edition, with the following publication details: Master Guide to Income Tax Act 2025—37th Edition | 2026; authored by Taxmann’s Editorial Board; spanning 1,800 pages across four Divisions; updated for the Finance Act 2026 Master Guide to Income Tax Rules 2026—33rd Edition | 2026; authored by Adv. M.K. Pithisaria and CA. Abhishek Pithisaria; over 1,700 pages covering all 333 rules; incorporates G.S.R. No. 198(E), dated 20-03-2026 Direct Taxes Ready Reckoner—50th Edition | Golden Jubilee Edition; authored by Dr Vinod K. Singhania; applicable to Assessment Year 2026-27 and Tax Year 2026-27; first published May 1978, commemorating fifty years of continuous annual publication under the same authorship The noteworthy features of this Combo are as follows: [First Authoritative Comparative Commentary on ITA 2025 vs. ITA 1961] Chapter-by-chapter, para-by-para comparative analysis across all 20 subject-matter areas of the new statute, with every para following a disciplined three-part structure—position under the ITA 1961, corresponding section in the ITA 2025, and a full analysis of the change including legislative intent, interpretive implications and practical consequences. The commentary explains why each change was made, whether it is substantive or merely structural, and where interpretive uncertainty survives despite the new drafting [Rule-wise Five-layer Treatise on the 2026 Rules] Every one of the 333 rules is treated as an independent commentary unit, analysed across five layers—statutory background tracing the parent provision in the 2025 Act, sub-rule-wise procedural commentary, tabulated lists of notified items and authorities, a dedicated comparison table identifying every divergence from the 1962 Rules, and Author’s Notes flagging interpretational gaps, drafting inconsistencies and silent areas [Finance Act 2026 Fully Integrated] All three titles incorporate Finance Act 2026 amendments directly into the running commentary at the point of relevance, with explicit editorial discipline distinguishing changes originating from the new statute versus the most recent Finance Act. Where the Finance Act 2026 has not amended a provision of the 2025 Act, the commentary explicitly notes this [Bidirectional Concordance Across Both Regimes] Four front-matter concordance tables in the Rules volume (1962 Rules ↔ 2026 Rules; 1962 Forms ↔ 2026 Forms) and an exhaustive bidirectional section-wise cross-reference index in the Ready Reckoner mapping every section of the 1961 Act to its corresponding provision in the 2025 Act at the paragraph level—enabling instant location of any provision under either Act [Complete TDS/TCS Reckoner Under the New Regime] Tabular reference covering every withholding provision under the ITA 2025 with nine column-heads (nature of income, payer category, payee category, threshold, rate where PAN/Aadhaar is furnished, rate where not furnished, time of deduction/collection), all fourteen exemption categories separately tabulated, the rationalised uniform 2% TCS structure, LRS tiered rates and overseas tour package differentials; supplemented by rule-by-rule procedural commentary on Rules 203–221 and pre-computed withholding rate tables across 100 provisions [Dual-Indexed CBDT and Judicial Compendia] Complete CBDT circulars, clarifications and notifications from 1961 through February 2026 and landmark Supreme Court and High Court rulings from 1922 through February 2026, each preceded by a section key mapped to ITA 2025 section numbers and an alphabetical key—preserving access to over a century of administrative and judicial guidance despite the renumbering of sections [Structural Transformation of the Statute Articulated] Systematic mapping of the architectural redesign of the statute—the elimination of ‘Previous Year’ and ‘Assessment Year’ in favour of the unified ‘Tax Year’, consolidation of NPO/trust provisions into a single dedicated chapter, recharacterisation of Section 10 exemptions as deductions, migration of 1,200 provisos and 900 explanations into sub-sections, clauses and sub-clauses, and the addition of five new schedules [Worked Numerical Case Studies and Multi-Scenario Analysis] Full numerical case studies on every Finance Act 2026 amendment, multi-scenario tax burden comparisons (voluntary disclosure, post-notice updated return, full reassessment, immunity), life insurance policy taxability matrix with consecutive case studies, the four new-regime rate categories under sections 199, 200, 201 and 202, and worked examples on shifts in limitation periods, investment thresholds, capital deployment timelines and valuation methodology [New vs. Old Tax Regime Parallel Analysis] All provisions presented in parallel for both regimes across every assessee category, with the four new-regime rate categories under sections 199, 200, 201 and 202 fully analysed—including eligible manufacturers (25%), default domestic companies (22% with fixed 10% surcharge and no MAT), new manufacturing companies (15%) and the default individual/HUF new regime with restricted exemptions and deductions [Pre-computed Tax Tables and Quick-reference Referencers] Eighteen Referencers covering tax rates, ICDS, depreciation, cost inflation index, withholding rates including DTAA, limitation periods, key compliance dates and the carry-forward of 1961 Act provisions into the 2025 Act framework; pre-computed tax liability tables for AY 2026-27/Tax Year 2026-27 by assessee category; and historical tax tables for the last six assessment years [Footnoted Citation System, Annexures and Integrated Guideline Material] Inline footnoted citations to the precise section, sub-section, clause, sub-clause, proviso and explanation of the 2025 Act, the corresponding 1961 Act provision, and the corresponding 1962 Rule and Form; supplemented by dedicated annexures attached to individual rules reproducing source CBDT circulars and notification material, and statutory guideline material reproduced in full where required —hospital approval guidelines, investment patterns for Recognised Provident Funds and Approved Superannuation Funds, electoral trust functioning norms and infrastructure debt fund setup conditions